Valid IIA-CIA-Part3 Dumps shared by ExamDiscuss.com for Helping Passing IIA-CIA-Part3 Exam! ExamDiscuss.com now offer the newest IIA-CIA-Part3 exam dumps, the ExamDiscuss.com IIA-CIA-Part3 exam questions have been updated and answers have been corrected get the newest ExamDiscuss.com IIA-CIA-Part3 dumps with Test Engine here:

Access IIA-CIA-Part3 Dumps Premium Version

(515 Q&As Dumps, 35%OFF Special Discount Code: freecram)

<< Prev Question Next Question >>

Question 22/152

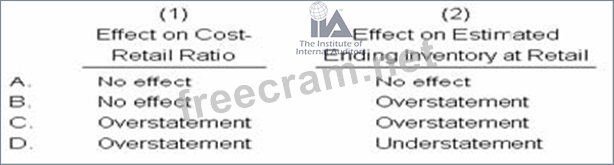

An entity uses the retail method of inventory estimation for interim reporting purposes.

Management expects some normal shrinkage in the inventory because of theft. What effect will the failure to consider this shrinkage have on the computation of1) the cost retail ratio, and2) the estimated ending inventory at retail?

Management expects some normal shrinkage in the inventory because of theft. What effect will the failure to consider this shrinkage have on the computation of1) the cost retail ratio, and2) the estimated ending inventory at retail?

Correct Answer: B

The retail method of inventory estimation applies a cost-retail ratio to the ending inventory at retail to determine ending inventory at cost For example, a popular method calculates the ratio as goods available for sale at cost divided by goods available at retail, with markups but not markdowns included in the calculation of the retail amount. Normal inventory is subtracted from the retail amount of goods available because are not available. However, abnormal amounts of theft, etc., are removed from the cost and retail amounts. The reason for the difference in treatment is that normal but not abnormal inventory losses are anticipated and included in the selling retail value). Accordingly, failure to account for normal inventory shrinkage has no effect on the calculate cost-retail ratio but overstates ending inventory at retail.

- Question List (152q)

- Question 1: A perpetual inventory system uses a minimum quantity on hand...

- Question 2: The Huron Corporation purchases 60,000 headbands per year. T...

- Question 3: A cost-volume-profit model developed in a dynamic environmen...

- Question 4: A cash flow hedge mitigates risk exposure due to variability...

- Question 5: Which stage in the industry life cycle is characterized by m...

- Question 6: The sales manager for a builder of custom yachts developed t...

- Question 7: With regard to e-commerce, risk is best defined as the uncer...

- Question 8: Which of the following principles are common to both hierarc...

- Question 9: At December 31, Year 1, an entity had the following equity a...

- Question 10: All of the following are true with regard to the first-in, f...

- Question 11: Which of the following are the most appropriate measures for...

- Question 12: Annual inventory holding costs equal:...

- Question 13: Which of the following techniques would be best for evaluati...

- Question 14: Market-skimming pricing strategies could be appropriate when...

- Question 15: Based on a comparison of RST's quick ratios in Year 5 and Ye...

- Question 16: Quality control programs employ many tools for problem defin...

- Question 17: The current generation of ERP software ERP II) may include a...

- Question 18: Total quality management (TQM) in a manufacturing environmen...

- 1 commentQuestion 19: An entity has the following contingencies at a balance sheet...

- Question 20: While auditing a marketing department, the internal auditor ...

- 1 commentQuestion 21: Which of the following is most important for an internal aud...

- Question 22: An entity uses the retail method of inventory estimation for...

- Question 23: The chart displays the:

- Question 24: Which of the following describes the most appropriate set of...

- Question 25: Dale has 20 days to complete production of an order for an i...

- Question 26: The leadership of an organization encourages employees to fo...

- Question 27: The average labor cost per unit for the first batch produced...

- Question 28: The share split proposal will <List A> earnings per sh...

- Question 29: In a traditional manufacturing operation, direct costs would...

- Question 30: If a call option is out-of-the-money, the:...

- Question 31: Which of the following statements is true regarding a bring-...

- Question 32: A competitive marketing strategy in which a firm specializes...

- Question 33: An example of an internal nonfinancial benchmark is:...

- Question 34: Which of the following conditions could lead an organization...

- Question 35: Organization X owns a 38 percent equity stake in Organizatio...

- Question 36: A company uses a target pricing and costing approach. The fo...

- Question 37: According to MA guidance on IT. which of the following best ...

- Question 38: During the past few gears, Wilder Company has experienced th...

- Question 39: Which of the following application software features is the ...

- Question 40: The drive-through service at a fast-food restaurant consists...

- Question 41: Which of the following assists in ensuring mat information e...

- Question 42: Which of me following is true of matrix organizations?...

- Question 43: Management of a bookkeeping company observed that the averag...

- Question 44: An audit manager has just returned from an executive trainin...

- Question 45: Assume that the average collection period is 25 days. After ...

- Question 46: The economic order quantity for inventory is higher for an o...

- Question 47: Which of the following budgets must be prepared first?...

- Question 48: A bank uses customer departmentalization to categorize its d...

- Question 49: An entity is subject to warranty claims. A reliable estimate...

- Question 50: At the end of September, a entity has outstanding accounts r...

- Question 51: Which of the following is not true of responsibility account...

- Question 52: A bank is developing a computer system to help evaluate loan...

- Question 53: Which of the following statements pertaining to a market ski...

- Question 54: A client installed the most sophisticated controls using bio...

- Question 55: The primary reason for adopting TOM was to achieve:...

- Question 56: Which line segment identifies the quantity of safety stock m...

- Question 57: Maintenance cost at a hospital was observed to increase as a...

- Question 58: How do data analysis technologies affect internal audit test...

- Question 59: A company is formulating its plans for the coming year, incl...

- Question 60: If Bandit Co. reports expenses on an accrual basis, interest...

- Question 61: The process of scenario planning begins with which of the fo...

- Question 62: When comparing absorption costing with variable costing, whi...

- Question 63: Tie-in sales e.g., the sale of camera and film together) mos...

- Question 64: The process of scenario planning begins with which of the fo...

- Question 65: Which of the following is a logical access control designed ...

- Question 66: An internal auditor observed that the organization's disaste...

- Question 67: Which of the following is true about the impact of price inf...

- Question 68: If a company is customer-centered, its customers are defined...

- Question 69: The ending inventory balance under the first-in, first-out-F...

- Question 70: An entity has a majority of its customers located in states ...

- 2 commentQuestion 71: Which of the following is a noncash item?...

- Question 72: If legal or regulatory standards prohibit conformance with c...

- 1 commentQuestion 73: Which of the following is most important for an internal aud...

- Question 74: Which of the following is a disadvantage in a centralized or...

- Question 75: Which of the following is not true about international trans...

- Question 76: According to the waterfall cycle approach to systems develop...

- Question 77: Which of the following IT controls includes protection for m...

- Question 78: Which of the following options correctly defines a transmiss...

- Question 79: Refer to the exhibit. (Exhibit) The figure below shows the n...

- Question 80: Which of the following statements is most accurate with resp...

- Question 81: An entity obtained a short-term bank loan of US $250,000 at ...

- Question 82: An internal auditor is assigned to perform data analytics. W...

- Question 83: Which of the following characteristics distinguishes compute...

- Question 84: Which of the following statements is true regarding outsourc...

- Question 85: Correlation is a term frequently used in conjunction with re...

- Question 86: An organization produces two products, X and Y. The material...

- Question 87: Which of the following methods, if used in conjunction with ...

- Question 88: Which of the following are included in ISO 31000 risk princi...

- Question 89: Which of the following are typical audit considerations for ...

- Question 90: The immediate goal of a theory of constraints (TOC) analysis...

- Question 91: A systems development approach used to quickly produce a mod...

- Question 92: Which of the following is the primary benefit of including e...

- Question 93: The calculation of an economic order quantity EOQ) considers...

- Question 94: At December 31, Year 2, an entity had the following obligati...

- Question 95: An organization accumulated the following data for the prior...

- Question 96: A U.S. company and a European company purchased the same sto...

- Question 97: IFPS 2, Share-Based payment, normally requires entities to a...

- Question 98: The amortization of intangible assets with finite useful liv...

- Question 99: The defined post employment benefit obligation of an entity ...

- Question 100: Organizations mat adopt just-in-time purchasing systems ofte...

- Question 101: The decision to implement enhanced failure detection and bac...

- Question 102: The credit instrument known as a banker's acceptance:...

- Question 103: A bank is designing an on-the-job training program for its b...

- Question 104: Which of the following statements is false regarding the eff...

- 1 commentQuestion 105: Which of the following authentication device credentials is ...

- 1 commentQuestion 106: An internal auditor was asked to review an equal equity part...

- Question 107: An internal auditor is reviewing physical and environmental ...

- Question 108: Violation of which assumption underlying regression analysis...

- Question 109: To mitigate a possible loss and offset risk, an entity can u...

- Question 110: When auditing an application change control process, which o...

- Question 111: Refer to the exhibit. If the profit margin of an organizatio...

- Question 112: Fulford Company applies the target pricing and costing appro...

- Question 113: According to MA guidance, which of the following best descri...

- Question 114: In Year 1, Company C introduced a new line of computer produ...

- Question 115: Good planning will help an organization restore computer ope...

- Question 116: The time that car 3 will have to wait to be serviced:...

- Question 117: As of week 8, the Gantt chart shows that the project is:...

- Question 118: An analysis of an entity's US $150,000 accounts receivable a...

- Question 119: The trough of a business cycle is generally characterized by...

- 1 commentQuestion 120: Which of me following responsibilities would ordinary fall u...

- Question 121: In a business combination, the sum of the amounts assigned b...

- Question 122: Changes in accounting estimates are viewed as:...

- Question 123: Presented below are partial year-end financial statement dat...

- Question 124: If Projects A and B. are independent, which of the following...

- Question 125: If legal or regulatory standards prohibit conformance with c...

- Question 126: The costs of quality that are incurred in detecting units of...

- Question 127: Using an EOQ analysis (assuming a constant demand), it is de...

- Question 128: Only two companies manufacture Product A. The finished produ...

- Question 129: If the bank uses the minimax regret criterion for selecting ...

- Question 130: An entity changes its method of accounting for depreciation ...

- Question 131: Which of the following statements is true regarding reversin...

- Question 132: Senior management has decided to implement the Three Lines o...

- Question 133: At the beginning of Year 1 a company began work on a 3-year ...

- Question 134: In an inventory system on a database management system DBMS)...

- Question 135: What is the economic term used to describe the situation in ...

- Question 136: A characteristic of the basic economic order quantity EOQ) m...

- 1 commentQuestion 137: Which of me following statements is true regarding the repor...

- Question 138: Heniser Pet Foods manufactures two products, X. and Y. The u...

- Question 139: A company purchased a new machine on an installment payment ...

- Question 140: An entity with total aside t, of US $100,000,000 and profit ...

- Question 141: A company has excess capacity in production-related fixed as...

- Question 142: Which of the following describes a typical desktop workstati...

- Question 143: Which of the following is a strategy that organizations can ...

- Question 144: Which of the following concepts of managerial accounting is ...

- Question 145: During the growth stage of a product's life cycle,...

- Question 146: Which of the following performance measures would be appropr...

- Question 147: Evaluating performance is not done to:...

- Question 148: An accounts payable program posted a payable to a vendor not...

- Question 149: The comparative balance sheet for an enterprise that had pro...

- Question 150: Quality cost indices are often used to measure and analyze t...

- Question 151: Business process reengineering is most likely to:...

- Question 152: Data access security related to applications may be enforced...